Photo credit: AvidOutdoorsman

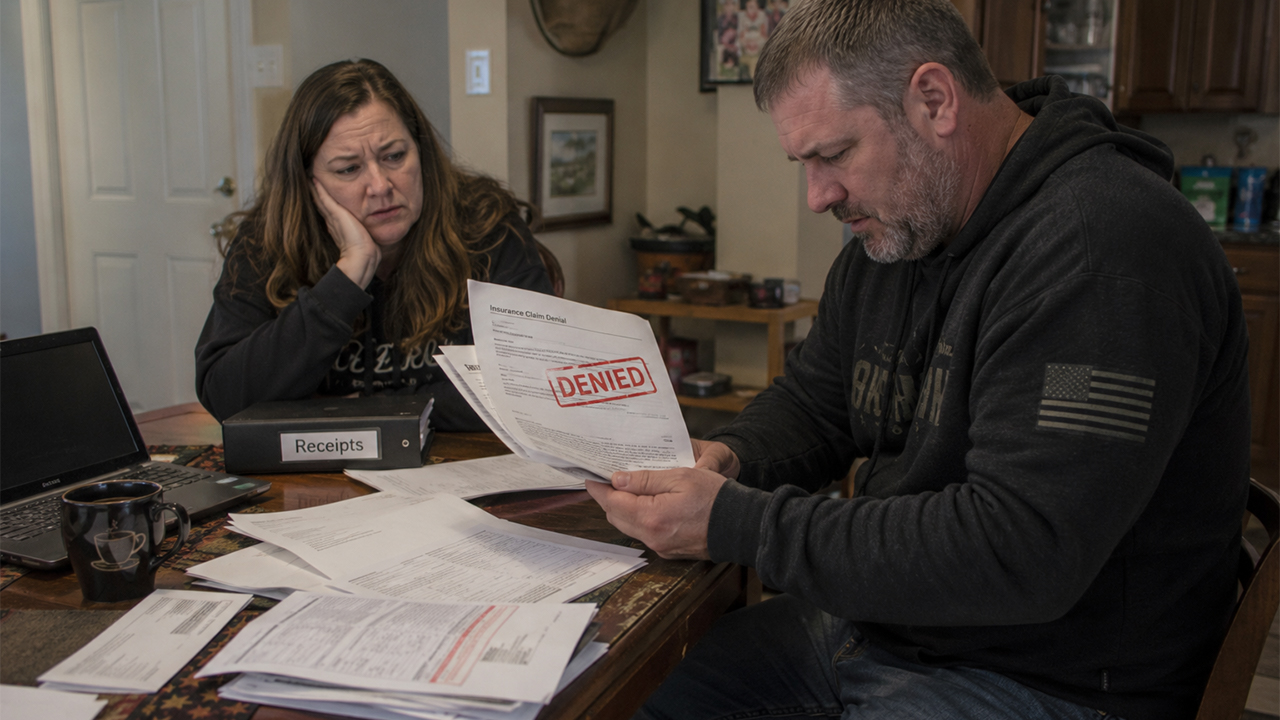

It’s a gut-punch feeling: you come home, something’s off, and your safe looks like it’s been picked clean. Not just one rifle missing, but the whole core of your hunting and home-defense setup—guns you’ve tuned, carried, and trusted for years. In this case, the owner did what most of us would do. He filed the police report, made a list, dug out serial numbers, and turned in a claim that added up to around twelve grand.

He didn’t wing it, either. He treated it like a range log. Every purchase receipt he could find went into the packet—firearms, optics, rings, cases, and the kind of “small stuff” that gets expensive fast. Then the insurance company came back with the kind of denial that makes your blood pressure rise: the policy, they said, didn’t cover firearms.

The claim was built the way insurers always tell you to build it

The owner’s side of the story looked solid on paper. A theft report, an itemized inventory, and proof of purchase is usually the holy trinity for personal property claims. A lot of folks can’t produce that after the fact, especially if they paid cash at a gun show ten years ago or swapped gear with a buddy.

This guy did the opposite. He kept receipts. He had serials. He could show what each item cost and when it was purchased, which is exactly what adjusters typically ask for when they start verifying value. If anything, it sounded like a “clean” claim—no vague numbers, no guessing, no inflated replacements.

Where things went sideways: a policy that treats guns differently than everything else

The denial didn’t come down to whether the theft happened or whether the items were real. It came down to language buried in the policy—one of those sections most people skim when they’re just trying to get the mortgage company happy or meet a landlord’s requirement.

A lot of standard homeowners and renters policies don’t treat firearms like regular household property. Some outright exclude them under certain endorsements, but more commonly they cap coverage at a low limit unless you schedule them. The owner heard “personal property covered for theft,” and assumed that meant the contents of his safe were included. The insurer pointed to the part that said “not so fast.”

That’s the part that stings. To a hunter or gun owner, a rifle is like a chainsaw or a welder—equipment. To an insurer, it can fall into the same bucket as jewelry, collectibles, or other high-theft items that they either limit or require extra paperwork for.

The receipts didn’t matter because coverage wasn’t the issue—exclusion was

People assume receipts are the key. They are, but only after you clear the first hurdle: whether the policy actually covers the category of property in the first place. If the contract says the item is excluded, you can hand them a three-ring binder of documentation and still end up with a denial.

This is where a lot of folks get tripped up. They’ll hear an agent say, “You’ve got X dollars of personal property coverage,” and they mentally assign that to the things they care about most—guns, bows, waders, trail cameras, and maybe a freezer full of meat. But contracts don’t care what you care about. They care what’s written.

In the gun world, that’s like finding out your optic warranty doesn’t cover what you assumed it covered. You can have the original box and purchase date, but if the fine print says “no electronics damage” or “no third-party mounts,” you’re still stuck.

Commenters zeroed in on two things: “scheduled items” and the agent conversation

Any time a denial like this hits the outdoors community, the same two camps show up. One camp says you should always “schedule” firearms. That means listing individual guns (often with serial numbers and values) on an endorsement or separate inland marine-style coverage so they’re insured specifically, sometimes even with broader protection.

The other camp focuses on the agent conversation: what was asked, what was promised, and what was put in writing. Plenty of people think they “told their agent about the guns,” and therefore they’re covered. But unless there’s an endorsement or a rider showing firearms coverage, that conversation can evaporate when the claim gets adjusted.

There’s also a third angle that pops up: storage and loss prevention. Some folks argue that a bolted-down safe, an alarm, and cameras should influence coverage decisions. In the real world, those things can reduce your chance of theft and may qualify for discounts, but they don’t rewrite exclusions.

What options a gun owner typically has after a denial like this

Denial doesn’t always mean dead end. If the owner believes the policy language was applied incorrectly, the first step is usually asking for the denial letter in writing with the exact policy section cited. Not a phone call summary—paperwork. Then you read it like you’d read a hunting regulation that doesn’t seem right.

Sometimes the issue is a misunderstanding: the policy may have a limit rather than a total exclusion. If there’s a sub-limit for firearms (for example, a few thousand dollars), the claim might be payable up to that cap. Other times, it’s truly excluded, and the only leverage is whether the policy was sold or renewed with misleading representations.

That’s where documentation matters again, just in a different way. Emails with the agent, quote proposals, declarations pages, and endorsements can show what the buyer reasonably believed they were purchasing. If it escalates, it can turn into a formal complaint process with the insurer, and sometimes beyond that. Nobody wants that hassle, but twelve grand is real money.

It also forces a hard look at replacement cost versus actual cash value. Even when coverage exists, some policies pay depreciated value unless you’ve got replacement-cost personal property. A ten-year-old shotgun might not get valued the way you’d value it, especially if it’s discontinued and the market is weird.

The practical lesson for hunters and gun owners: insure the safe, not the idea of the safe

This is one of those stories that changes how you look at your own setup. If you’ve got a couple of budget rifles and a pump shotgun, maybe your existing policy limit is enough. But a lot of us don’t live there anymore. A decent scoped deer rifle, a turkey gun with an optic, a carry pistol, and a .22 can stack up fast. Add suppressors where legal, optics, and a few quality handguns, and you can hit five figures without trying.

The fix isn’t complicated, but it does take discipline. Inventory what you own. Photograph it. Record serial numbers. Store that information somewhere offsite or in a secure digital vault. Then call your agent and ask a pointed question: “Are firearms excluded, limited, or fully covered? And what endorsement covers them?” If they can’t point to the form number and the line item on your declarations page, assume you’re not covered the way you think you are.

It’s the same mindset as checking your zero before season. You don’t wait until opening morning to learn something shifted. Insurance is no different. The time to find out what’s excluded isn’t after your safe is empty.

Like The Avid Outdoorsman’s content? Be sure to follow us.

Here’s more from us: